When a lender tells us their leads “aren’t converting,” we’ve learned to ask a different question before we look at the lead source: What happens in the first five minutes after the lead comes in?

The answer is almost always where the money is leaking.

Here’s the uncomfortable math. The Mortgage Bankers Association puts the all-in cost to produce a single loan at $11,076 in 2024 — and net production income at just $443 per loan.1 When margins are that thin, the difference between a lead that funds and a lead that dies in a CRM queue isn’t a rounding error. It’s the whole business.

The good news: the highest-ROI fixes have nothing to do with buying more leads or better leads. They’re about how fast, how persistently, and how accountably you work the leads you already pay for. None of the seven moves below require new budget. Most can be live this week.

First, understand what you’re actually working

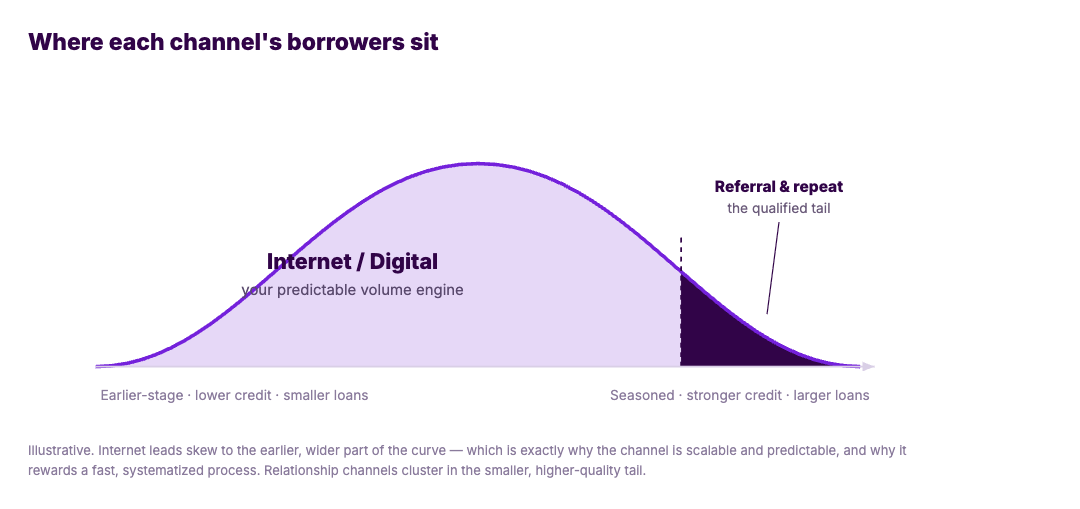

One framing changes everything: internet leads are not the leads your team is used to working.

Most loan officers cut their teeth on referrals, repeat clients, Realtor partnerships, direct mail, and credit-trigger leads. Those borrowers arrive warm, pre-qualified by a trusted relationship, often further along and more financially seasoned. So when an LO applies that same instinct to an internet lead — a slow, consultative, “they’ll call me back” approach — it fails, and everyone blames the lead.

The honest truth about real-time internet leads is that they skew toward the wider, earlier end of the bell curve: less experienced borrowers, earlier in their journey, frequently lower credit and smaller loan amounts, and almost always shopping more than one lender at the same moment. That’s not a defect — it’s the nature of the channel.

And here’s why it’s worth mastering anyway: internet lead generation is predictable, scalable, and sustainable in a way relationship channels never can be. You can’t manufacture more Realtor referrals on demand, and direct mail and credit triggers are episodic and increasingly constrained. Digital is a faucet you can turn up. It’s no accident that the largest modern lenders — Rocket chief among them — were built on direct-to-consumer internet lead generation. Worked correctly, it becomes the foundational marketing channel the rest of your pipeline sits on top of.

The catch is right there in the bell curve: because the borrower is earlier and shopping harder, the lender who responds first, fastest, and most persistently wins — far more so than in any relationship channel. That single difference is why the rest of this checklist exists.

| Referral / Repeat | Direct Mail | Credit Triggers | Internet / Digital | |

|---|---|---|---|---|

| Borrower intent | High — ready, trusts you | Moderate — prompted by an offer | Moderate — rate-shopping | Early & exploratory |

| Experience & profile | Seasoned, stronger credit | Mixed | Mixed, often refi-minded | Newer, lower credit, smaller loans |

| Competition at first touch | Low — you’re the trusted name | Moderate | High — many lenders at once | Highest — shopping several now |

| Volume predictability | Unpredictable | Episodic (campaign-based) | Episodic, regulation-sensitive | Predictable & dial-up/down |

| Scalability | Hard to scale | Capital- & list-limited | Limited & constrained | Highly scalable |

| Speed-to-lead sensitivity | Low — they’ll wait | Moderate | High | Decisive — minutes matter |

| How to work it | Consultative, relationship-paced | Offer-led follow-up | Fast, rate-focused | Instant, persistent, system-driven |

These channels aren’t rivals — they’re a portfolio. Referrals and repeat business are your highest-margin work; internet is the predictable engine that fills the calendar between them and feeds tomorrow’s referral and repeat pipeline. But you can only realize that if you stop working internet leads like referrals. That’s what the seven moves below are for.

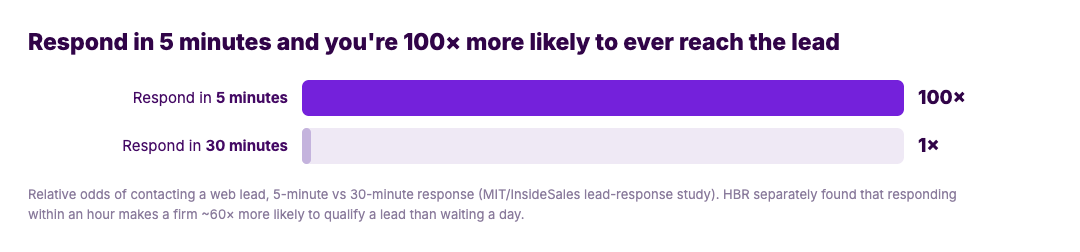

1. First contact in 5 minutes, not 5 hours

This is the single highest-leverage lever in the entire funnel, and it’s the one most lenders quietly fail.

The landmark MIT lead-response study (Dr. James Oldroyd, analyzing 15,000+ leads and 100,000+ call attempts) found that the odds of contacting a web lead are 100x higher when you respond within 5 minutes versus 30 minutes — and the odds of qualifying that lead are 21x higher.2 Harvard Business Review’s follow-up research found firms that respond within an hour are 7x more likely to have a meaningful conversation than those who wait just one hour longer — and 60x more likely than firms that wait a day.3

Now the gut-punch: that same HBR audit found the average company took 42 hours to respond, and 23% never responded at all.3

Do this Monday: Time-stamp your last 20 internet leads from arrival to first response. If your median is over 5 minutes, you have your first project. The fix is rarely “hire faster people” — it’s automation that fires the instant a lead hits the form (that’s #2, and it’s the most important move on this list).

A note on what the data does and doesn’t say: these studies measured contacting and qualifying leads across many industries — not mortgage close rates specifically. Treat speed as what gets you in the door, not a guarantee of the loan.

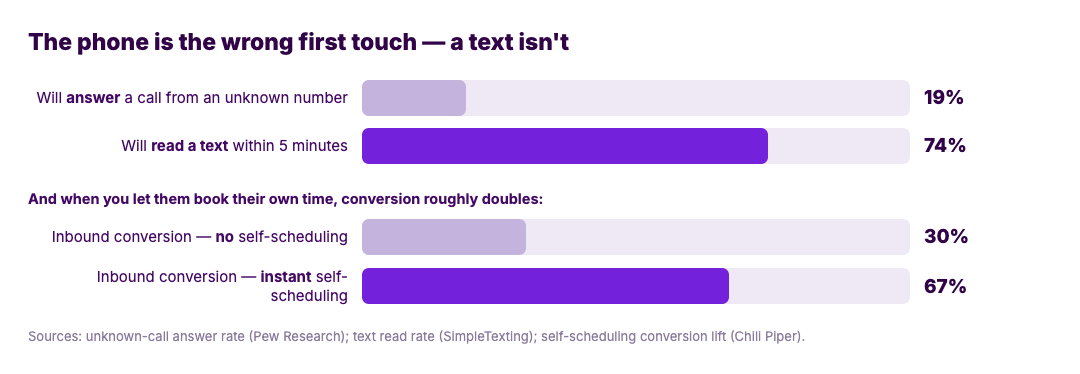

2. Make the first touch an automated text — not a cold call

If you do only one thing on this list, do this one. The instant a lead hits your form, fire an automated, branded text — before a human lifts a finger. It’s the highest-impact, easiest-to-implement move you can make, and it solves the speed problem in #1 by default.

Here’s why it beats a call: your prospect won’t pick up the phone. 81% of Americans don’t answer calls from unknown numbers.4 A text does the opposite — 74% of consumers read a text within five minutes,5 and when they have a question, more of them would rather text a business than call it.5 So the highest-converting first touch is an instant text — “Hi [name], it’s [LO] at [lender], I’ve got your rate request” — paired with a link that lets them book a time themselves.

That scheduling link matters more than it looks. 74% of consumers now expect to handle anything online that they could by phone6 — they want to control their own time, not sit by the phone waiting for a callback. Hand them the controls and they convert: businesses that let a lead self-book a meeting immediately after a form-fill roughly double their inbound conversion, from 30% to 67%.7

This is also the cleanest division of labor. Software can fire that text and scheduling link in seconds, 24/7 — a person at a desk never can. So let systems own the instant first touch, and reserve your loan officers for the booked call, where trust is actually built. You earn the call; you don’t cold-pounce it.8

Do this Monday: Stand up an automated, branded text plus a self-scheduling link that fires within seconds of every new internet lead — not a queued call — and make sure a booked time routes to the right LO with the lead’s details in hand. (Building that text-and-scheduling first touch and the routing behind it is core to the speed-to-lead systems we set up for lenders at Kaleidico.)

3. Commit to a 6-touch cadence — because attempt #1 almost never connects

Most loan officers call once, maybe twice, mark the lead “no answer,” and move on. That habit throws away the majority of the leads you bought.

Velocify’s analysis of millions of leads found that 93% of leads that eventually convert are reached by the sixth call attempt — and recommends a structured cadence of roughly 6 calls and 5 emails over the working life of a lead.9 The lesson isn’t “dial forever.” It’s that giving up at attempt two leaves most of your reachable pipeline on the table.

Do this Monday: Write down your actual required cadence — number of calls, texts, and emails, and over how many days — and make it the default in your CRM. If it isn’t written and enforced, it isn’t happening. (This cadence research is cross-industry; use it as a floor for discipline, not a mortgage-specific guarantee.)

4. Call when buyers actually pick up

You can’t control whether someone answers, but you can stop calling into dead air. The MIT data identified clear patterns: Wednesday and Thursday are the strongest days to reach leads, and the late-afternoon window (roughly 4–6 PM) consistently beats midday for making contact.2 Independent modern call-data analyses point to the same Wednesday / late-afternoon sweet spot.10 This is a free optimization — it just reallocates effort you’re already spending.

Do this Monday: Have LOs front-load their fresh-lead and follow-up calling into the late-morning and late-afternoon windows midweek, instead of spreading dials evenly (or burning them on Monday mornings and Friday afternoons).

5. Treat the CRM as the system of record — not a graveyard

A lead with no disposition is a lead you paid for and then threw away. The leak here is invisible because nothing shows up as “lost” — leads just quietly stop getting worked. The discipline is simple: every lead has a status, an owner, and a next action with a date. No exceptions. If a sales director can’t open the CRM and see exactly what’s happening with every lead bought this month, the leaks can’t be found, let alone fixed.

Do this Monday: Pull a report of leads from the last 30 days with no activity logged in the past 7 days. That number is your accountability gap, in dollars.

6. Build a real nurture track — most of your leads aren’t ready today

The instinct to chase only the hot, ready-now leads quietly discards the larger half of what you paid for. Research consistently finds roughly half of all leads are qualified but not yet ready to buy,11 and that companies who nurture well generate 50% more sales-ready leads at 33% lower cost.12

In mortgage this matters twice over, because the relationship doesn’t end at funding. Black Knight data shows lender retention has collapsed to around 18% — meaning four of five borrowers you funded take their next loan somewhere else.13 A database you don’t nurture is repeat business you’re handing to a competitor.

Do this Monday: Make sure leads that don’t convert in 30 days drop into an automated long-term nurture (rate-market touches, helpful content, periodic check-ins) — and that past closings are in it too. Recycle leads; don’t delete them.

7. Manage to cost-per-funded-loan, not cost-per-lead

This is the mindset shift that makes the other six stick. When you measure cost-per-lead, every conversation is about buying leads cheaper. When you measure cost-per-funded-loan, the conversation becomes about converting better — which is where your real leverage is.

A lender paying more per lead but converting at twice the rate is running a more profitable operation than the one chasing the cheapest leads. Tie it back to that MBA number: at ~$11,076 of total cost per loan,1 squeezing one more funded loan out of leads you’ve already bought is worth far more than shaving a few dollars off lead cost.

Do this Monday: Start tracking one new number per lead source — funded loans ÷ total spend on that source. Rank your sources by that, not by lead price. The cheapest source rarely wins.

The pattern

Six of these seven moves cost nothing but discipline. They’re about speed, persistence, accountability, and measuring the right number — applied to leads you’ve already paid for. That’s almost always a bigger, faster ROI win than another lead-source experiment.

Want a gut-check on where your leads are leaking?

We help mortgage lenders generate the leads — and build the speed-to-lead automation and CRM accountability that turn them into funded loans.

Sources

- Mortgage Bankers Association, Quarterly Mortgage Bankers Performance Report (Marina Walsh, CMB). Full-year 2024 total loan production cost of $11,076 and net production income of $443/loan. Source — total all-channel origination cost per loan, not marketing or lead cost.

- Dr. James Oldroyd (MIT Sloan) & InsideSales.com, Lead Response Management Study, 2007 (15,000+ leads, 100,000+ call attempts). 100x contact / 21x qualify advantage at 5 vs 30 minutes; best contact days Wed/Thu; best window ~4–6 PM. Source — measured contact and qualification, cross-industry web leads.

- Oldroyd, McElheran & Elkington, “The Short Life of Online Sales Leads,” Harvard Business Review, March 2011. 7x within the hour; 60x vs 24+ hours; average response 42 hours; 23% never responded. Source

- Pew Research Center, “Most Americans don’t answer cellphone calls from unknown numbers,” Dec 2020 (10,211 U.S. adults). 81% do not generally answer calls from unknown numbers. Source

- SimpleTexting, SMS Marketing Statistics 2026 (1,000 U.S. consumers). 74% read a text within 5 minutes; more consumers prefer to text a business (33%) than call it (18%). Source

- Salesforce, State of the Connected Customer, 6th ed. (14,300 respondents, 2023). 74% expect to do anything online that they could in person or by phone. Source

- Chili Piper, 2025 Benchmark Report on Demo Form Conversion Rates (~4M form submissions). Instant self-scheduling raised average inbound conversion from 30% to 66.7%. Source — Chili Piper’s own (largely B2B) customer data; directional.

- HowToWorkLeads, How to Build a Real-Time Internet Lead Team — on the text-first, self-scheduling, “earn the call” engagement model. Source

- Velocify (now ICE Mortgage Technology), The Ultimate Contact Strategy (~3.4M leads). 93% of converted leads reached by the 6th call; cadence of 6 calls + 5 emails. Source — cross-industry data.

- CallHippo, Best Day & Time to Make Business Calls (52,000+ calls). Wednesday and late-afternoon windows perform best for connecting. Source

- Gleanster Research, via HubSpot — roughly 50% of leads are qualified but not yet ready to buy. Source

- Forrester Research, via HubSpot — companies that excel at lead nurturing generate 50% more sales-ready leads at 33% lower cost. Source

- Black Knight Mortgage Monitor (Jan 2021), via STRATMOR Group — overall lender retention fell to ~18%. Source